2020年CFA考试《CFA一级》章节练习题精选0413

2020年CFA考试《CFA一级》考试共240题,分为单选题。小编为您整理Derivative Investments5道练习题,附答案解析,供您备考练习。

1、An analyst does research about currency swap and gathers the followinginformation about a dollar-euro currency swap in which both parties pay afixed rate:

If both payments are quarterly and made on the basis of 30 days per month and365 days per year, the final amount exchanged at the end of the swap areclosest to:【单选题】

A.$ 90 million and € 70 million.

B.$ 91.15 million and € 71.10 million.

C.$ 91.42 million and € 70.89 million.

正确答案:B

答案解析:最后交换时要加上每期的支付,即 $ 90 million ×(1 +5.1%/4) = $ 91.15 million,另一方则是€70 million × (1 +6.3%/4) =€71.10 million。

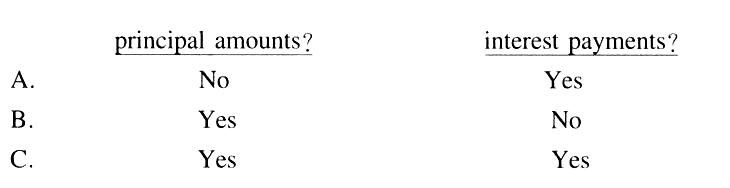

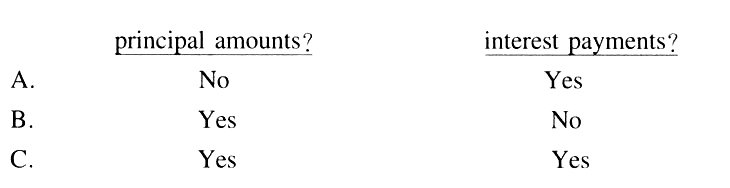

2、An analyst does research about currency swap and stated that, in the typical currencyswap, principal amounts are exchanged at both the beginning and end ofthe swap and interest payments are netted during the life of the swap.The analystis most accurate with respect to :【单选题】

A.

B.

C.

正确答案:B

答案解析:货币互换是两种不同的货币之间的相互交换,通常本金在期初期末要进行交换,期间的利息支付不可以相互抵消。

3、An analyst does research about a forward agreement (FRA).A FRA is referredto as a 3 ×9.The terms of the agreement are a:【单选题】

A.3-month rate and a 6-month expiration.

B.3-month rate and a 9-month expiration.

C.6-month rate and a 3-month expiration.

正确答案:C

答案解析:本题考的是一个远期利率协议的基本概念,这里面的“3”指的是从现在起3个月之后协议截止,开始利率交换;“9”则指从现在起9个月之后利率交换全部结束,所以远期利率协议的期限是3个月,针对的是6个月的利率。

4、A buyer would face the greatest risk of default with:【单选题】

A.a farmer making physical delivery on a short soybean futures position.

B.an investment bank making cash settlement on a short euro futures position.

C.a multinational firm making cash settlement on a short U.S. dollar forward contract.

正确答案:C

答案解析:“Futures Markets and Contracts,” Don M. Chance

2011 Modular Level I, Vol. 6, p. 53

Study Session 17-62-b

Compare futures contracts and forward contracts.

C is correct because in a forward contract, each party assumes the risk that the other party will default.

5、An investor enters into a 1 x 3 forward rate agreement at a LIBOR rate of 1.5%. At expiration, the 60-day LIBOR rate is 1.7% and the 90-day LIBOR rate is 1.6%. Assuming the contract covers a $1 million notional principal, what payment will the investor most likely receive?【单选题】

A.$249.00

B.$332.39

C.$333.33

正确答案:B

答案解析:$1 million × {(0.017–0.015)(60/360)/[1+ 0.017(60/360)]} = $332.39.

2014 CFA Level I

"Forward Markets and Contract," by Don M. Chance

Section 3.2.2