2020年CFA考试《CFA一级》每日一练

2020年CFA考试《CFA一级》考试共240题,分为单选题。小编每天为您准备了5道每日一练题目(附答案解析),一步一步陪你备考,每一次练习的成功,都会淋漓尽致的反映在分数上。一起加油前行。

1、Alexander Newton, CFA, is the chief compliance officer for Mills Investment Limited. Newton institutes a new policy requiring the pro rata distribution of new security issues to all established discretionary accounts for which the new issues are appropriate. The policy also provides for the distribution of new issues to newly established discretionary accounts where appropriate after their one-month anniversary date. This policy is disclosed to all existing and potential clients. Did Newton violate any CFA Institute Standards of Professional Conduct?【单选题】

A.No.

B.Yes, because the distribution policy should treat all discretionary accounts equally.

C.Yes, because disclosure of inequitable allocation methods does not fulfill the duty for fair and equitable trade allocation procedures.

正确答案:C

答案解析:“Guidance for Standards I-VII”, CFA Institute

2010 Modular Level I, Vol. 1, pp. 53-58

Study Session 1-2-a

Demonstrate a thorough knowledge of the Code of Ethics and Standards of Professional Conduct by applying the Code and Standards to situations involving issues of professional integrity.

Standard III (B) Fair Dealing requires when making investments in new offerings, advance indications of interest should be obtained as well as, providing for a method for calculating allocations. Additionally, disclosure of inequitable allocation methods does not relieve a member from this obligation.

2、An investor currently has a portfolio valued at $700,000. The investor’s objective is long-term growth, but she will need $30,000 by the end of the year to pay her son’s college tuition and another $10,000 by year-end for her annual vacation. The investor is considering three alternative portfolios:

Using Roy’s safety-first criterion, which of the alternative portfolios most likely minimizes the probability that the investor’s portfolio will have a value lower than $700,000 at year-end?【单选题】

A.Portfolio 2

B.Portfolio 3

C.Portfolio 1

正确答案:B

答案解析:The investor requires a minimum return of ($30,000 + $10,000)/$700,000, or 5.71%. Roy’s safety-first model uses the excess portfolio’s expected return over the minimum return and divides that excess by the standard deviation for that portfolio:

The portfolio with the highest safety-first ratio minimizes the probability that the investor’s portfolio will have a value lower than $700,000 at year end. The highest safety-first ratio is associated with Portfolio 3: 0.3768.

2014 CFA Level I

“Common Probability Distributions,” by Richard A. DeFusco, Dennis W. McLeavey, Jerald E. Pinto, and David E. Runkle

Section 3.3

3、An analyst does research about net profit margin.A company has only fixedrate debt outstanding and reports its debt using the fair value option.Whichof the following statements is most accurate when market interest rates decrease?【单选题】

A.The company's net profit margin decreases.

B.The company's net profit margin remains the same.

C.The company's net profit margin increases.

正确答案:A

答案解析:由于公司的负债都是固定利率,而市场利率下降,所以公司负债的公允价值也会上升并导致相应的损失,使得净利润减少,净利润率下降。

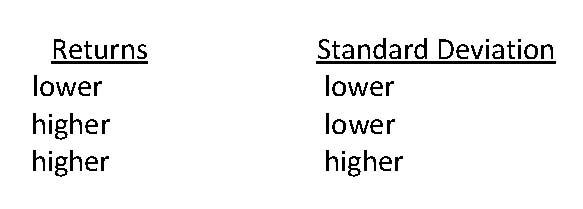

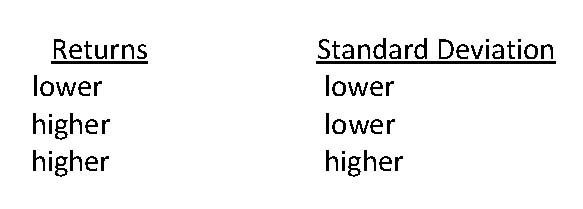

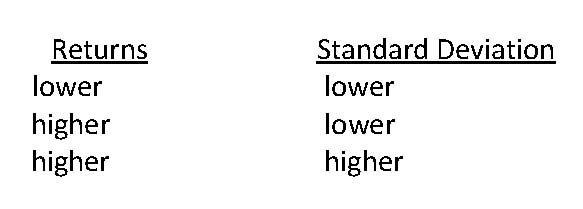

4、Adding alternative investments to a portfolio of traditional investments will most likely result in a new combined portfolio with returns and standard deviation that are, respectively:【单选题】

A.

B.

C.

正确答案:B

答案解析:“Introduction to Alternative Investments”, Terri Duhon, George Spentzos, CFA, and Scott D. Stewart, CFA

2013 Modular Level I, Vol. 6, Reading 66, Section 2.3

Study Session 18-66-c

Describe potential benefits of alternative investments in the context of portfolio management.

B is correct because the risk/return profile of the overall portfolio will potentially improve. The overall risk will most likely drop, and the overall return will most likely rise.

5、An analyst determines that a 5.50 percent coupon option-free bond, maturing in 7 years, would experience a 3 percent decrease in price if market interest rates rise by 50 basis points. If market interest rates instead fall by 50 basis points, the bond’s price would increase by:【单选题】

A.exactly 3%.

B.less than 3%.

C.more than 3%.

正确答案:C

答案解析:“Introduction to the Measurement of Interest Rate Risk,” Frank J. Fabozzi

2010 Modular Level I, Vol. 5, pp. 524-528

Study Session 16-66-b

Demonstrate the price volatility characteristics for option-free, callable, prepayable, and putable bonds when interest rates change.

The bond is option-free and will therefore exhibit positive convexity. An equal change in rates will produce a greater percentage gain when rates decrease than the percentage loss produced when rates increase.