2020年CFA考试《CFA一级》章节练习题精选

2020年CFA考试《CFA一级》考试共240题,分为单选题。小编为您整理Fixed Income Investments5道练习题,附答案解析,供您备考练习。

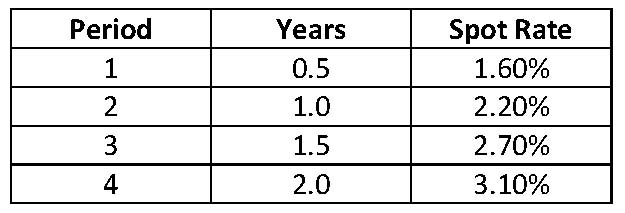

1、Using the U.S. Treasury spot rates provided below, the arbitrage-free value of a 2-year Treasury, $100 par value bond with a 6% coupon rate is closest to: 【单选题】

【单选题】

A.$99.75.

B.$105.65.

C.$107.03.

正确答案:B

答案解析:“Introduction to the Valuation of Debt Securities,” Frank J. Fabozzi

2012 Modular Level I, Vol. 5, pp. 504–506

Study Session 16-57-f

Explain and demonstrate the use of the arbitrage-free valuation approach, and describe how a dealer can generate an arbitrage profit if a bond is mispriced.

B is correct because the value of the bond is

2、The yield of a U.S. bond issue quoted on a bond-equivalent basis is 6.8 percent. The yield-to-maturity on an annual-pay basis is closest to:【单选题】

A.6.69%.

B.6.92%

C.14.06%.

正确答案:B

答案解析:“Yield Measures, Spot Rates, and Forward Rates”, Frank J. Fabozzi, CFA

2010 Modular Level I, Vol. 5, pp. 457

Study Session 16-65-d

Compute and interpret the bond equivalent yield of an annual-pay bond, and the annual-pay yield of a semiannual-pay bond.

B is correct because the yield on an annual-pay basis is calculated as:

The yield on an annual-pay basis is always greater than the yield on a bond-equivalent basis because of compounding.

3、Which of these embedded options most likely benefits the investor?【单选题】

A.The floor in a floating-rate security

B.An accelerated sinking fund provision

C.The call option in a fixed-rate security

正确答案:A

答案解析:“Features of Debt Securities,” Frank J. Fabozzi

2012 Modular Level I, Vol. 5, p. 337

Study Session 15-53-e

Identify common options embedded in a bond issue, explain the importance of embedded options, and identify whether such options benefit the issuer or the bondholder.

A is correct because the floor guarantees a minimum rate the investor will earn.

4、An analyst does research about duration.If the interest rate falls by 25 basispoints, the price of a bond will be $ 106.5, and if interest rate rises by 25 basispoints, the price of the bond will be $ 98.8.If the current price of thebond is $ 101.2, the duration is closest to:【单选题】

A.7.61

B.15.22

C.30.44

正确答案:B

答案解析:$ (106.5 - 98.8)/(2 × $ 101.2 × 0.0025) = $ 15.22。

5、When compared with an option-free bond, which type of bond most likely offers a higher yield to bondholders?【单选题】

A.Callable

B.Convertible

C.Putable

正确答案:A

答案解析:A callable bond gives the issuer the right to buy back the bond prior to maturity. This feature increases the reinvestment risk faced by bondholders, causing them to require a higher yield than for a similar non-callable bond.

2014 CFA Level I

"Fixed-Income Securities: Defining Elements," by Moorad Choudhry and Stephen E. Wilcox

Sections 5.1 – 5.3