2020年CFA考试《CFA一级》章节练习题精选

2020年CFA考试《CFA一级》考试共240题,分为单选题。小编为您整理Portfolio Management5道练习题,附答案解析,供您备考练习。

1、Last year, a portfolio manager earned a return of 12%. The portfolio’s beta was 1.5. For the same period, the market return was 7.5% and the average risk-free rate was 2.7%. Jensen’s alpha for this portfolio is closest to:【单选题】

A.0.75%.

B.2.10%.

C.4.50%.

正确答案:B

答案解析:“Portfolio Risk and Return Part II,” Vijay Singal

2012 Modular Level I, Vol. 4, pp. 429–432

Study Session 12-45-h

Describe and demonstrate applications of the CAPM and the SML.

B is correct. Jensen’s alpha = 0.12 – [0.027 + 1.5(0.075 – 0.027)] = .021 or 2.10%.

2、A portfolio with equal parts invested in a risk-free asset and a risky portfolio will most likely lie on:【单选题】

A.the efficient frontier.

B.the security market line.

C.a capital allocation line.

正确答案:C

答案解析:“Portfolio Risk and Return: Part II”, by Vijay Singal.

2011 Modular Level I, Vol. 4, pp. 392-400

Study Session 12-53-b

Explain and interpret the capital allocation line (CAL) and the capital market line (CML).

C is correct. A capital allocation line shows possible combinations of a risky portfolio and the risk-free asset.

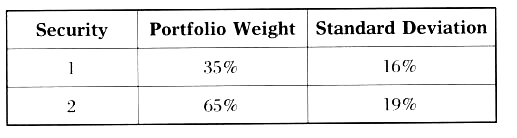

3、An analyst does research about the portfolio's standard deviation of return.Aportfolio consisting of two securities has the following characteristics:

If the correlation of returns between the two securities is -0.25, the portfolio'sstandard deviation of return is closest to:【单选题】

A.12.22%

B.14.78%

C.14.93%

正确答案:A

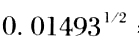

答案解析:投资组合的方差 - 2 × 0.35 × 0.55 × 0.16 × 0.19 × 0.25 = 0.00314 +0.01525 - 0.00346 = 0.01493。

- 2 × 0.35 × 0.55 × 0.16 × 0.19 × 0.25 = 0.00314 +0.01525 - 0.00346 = 0.01493。

投资组合的标准差 =  = 12.22%。

= 12.22%。

4、Concentrated portfolio strategies are attractive because of their:【单选题】

A.ability to track market indices.

B.low risk.

C.potential to generate alpha.

正确答案:C

答案解析:Concentrated portfolio strategies focus on only a few securities, strategies, or managers. This focusreduces diversification but may enable investors to achieve alpha.

CFA Level I

"Introduction to Alternative Investments," Terri Duhon, George Spentzos, and Scott D. Stewart

Section 2.2

5、An analyst does research about investment risk.Which of the following statementsbest describes systematic risk?【单选题】

A.Total risk.

B.Diversifiable risk.

C.Variability in all risky assets caused by macroeconomic variability.

正确答案:C

答案解析:非系统性风险是可分散化的风险。系统性风险是宏观经济等因素对所有风险性资产所造成的风险,是无法分散化的风险。总风险是非系统性风险和系统性风险的总和。