2020年CFA考试《CFA一级》章节练习题精选

2020年CFA考试《CFA一级》考试共240题,分为单选题。小编为您整理Fixed Income Investments5道练习题,附答案解析,供您备考练习。

1、An analyst does research about option-free bond price change due to both durationand convexity impacts.The duration of an option-free bond is 9.92, andthe convexity measure for that bond is 63.8.If interest rates increase by 200 basispoints, the bond's percentage price change is closest to:【单选题】

A.-22.39%

B.-18.56%

C.-17.29%

正确答案:C

答案解析:-9.92 ×2% +63.8 ×  = -17.29%。

= -17.29%。

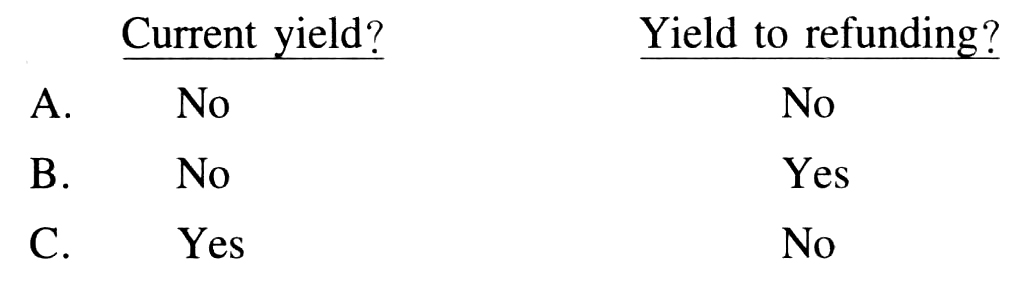

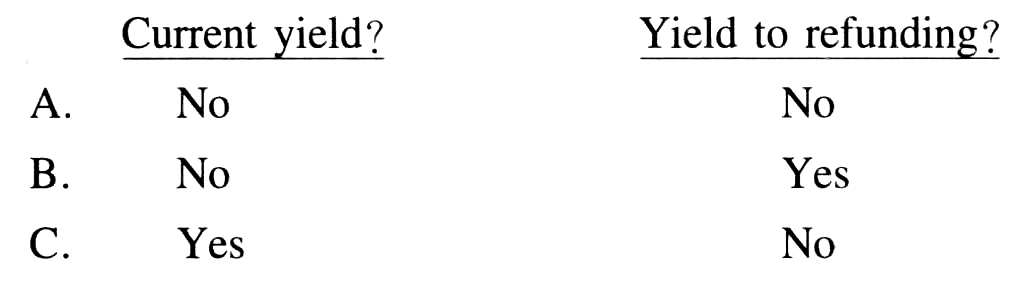

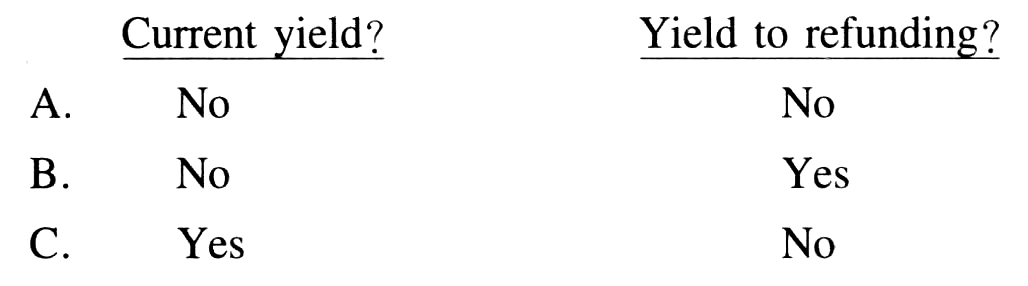

1、An analyst does research about various bond yields.An analyst stated that computingboth a bond's current yield and a bond's yield to refunding assumes thatall interim cash flows from the bond are reinvested at that bond's yield to maturity.Is the analyst correct with respect to interim cash flows and computinga bond's:【单选题】

A.

B.

C.

正确答案:A

答案解析:当前收益率(Current yield)不考虑已经产生的现金流的再投资,而再融资收益率(Yieldto refunding)将被作为之前获得的现金流再投资的收益率,而不是将持有到期收益率(YTM)作为再投资的收益率。再融资收益率是在到期之前通过重新融资把之前的债券提前偿还而产生的收益率。

1、An analyst does research about the basic theories of the term structure.Accordingto liquidity preference theory, the term structure of interest rates is leastlikely determined by:【单选题】

A.expectations about future interest rates.

B.a yield premium for interest rate risk.

C.preference for particular maturity range.

正确答案:C

答案解析:根据流动性偏好理论,其利率期限结构是由未来利率的预期加上持有长期债券的利率风险的补偿所组成的。投资者拥有其偏好的期限是属于市场分割理论的特征。

1、A long-term bond investor with an investment horizon of 8 years invests in option-free, fixed-ratebonds with a Macaulay duration of 10.5. The investor most likely currently has a:【单选题】

A.positive duration gap and is currently exposed to the risk of lower interest rates.

B.negative duration gap and is currently exposed to the risk of higher interest rates.

C.positive duration gap and is currently exposed to the risk of higher interest rates.

正确答案:C

答案解析:The duration gap is the bond's Macaulay duration minus the investment horizon, which is positive inthis case. A positive duration gap implies that the investor is currently exposed to the risk of higherinterest rates.

CFA Level I

"Understanding Fixed-Income Risk and Return", James F. Adams and Donald J. Smith

Section 4.2

1、When are credit spreads most likely to narrow? During:【单选题】

A.economic expansions.

B.economic contractions.

C.a period of flight to quality.

正确答案:A

答案解析:“Understanding Yield Spreads,” Frank J. Fabozzi, CFA

2013 Modular Level I, Vol. 5, Reading 55, Section 4.3

Study Session 15-55-f

Describe credit spreads and relationships between credit spreads and economic conditions.

A is correct. Credit spreads narrow during economic expansions and widen during economic contractions. During an economic expansion, corporate revenues and cash flows rise, making it easier for corporations to service their debt, and investors purchase corporates instead of Treasuries, thus causing spreads to narrow.